The Future of Embedded Payments in Australia

Embedded payments is fast gaining traction in the local APAC market, and is quickly becoming the new frontier for elevated customer experiences and value creation within software platforms.

With rapid uptake across both B2B and B2C software platforms, in-platform payments presents a unique opportunity for local software providers to differentiate and expand their reach and potential. For APAC businesses wanting to expand globally, embedded payments can also be the ‘key’ to unlocking new markets and expansion.

And with overseas markets, such as the USA, further along their embedded payments journey, Australia’s integrated payments market is at an inflection point – driven by changing policy, updated compliance regulations, and the rapid growth in demand for cashless payments in the last three years.

This article details how Australia differs from other global markets in payment facilitation and how APAC software businesses can use embedded finance for stronger revenue growth and customer retention.

Australia’s integrated payments market is at an inflection point – driven by changing policy, updated compliance regulations, and the rapid growth in demand for cashless payments…

What is embedded finance and embedded payments?

Embedded finance uses financial tools and services to make the processing/financing of purchases and payment facilitation seamless. These tools and services form part of a wider service offering through what’s known as “banking as a service” (BaaS).

BaaS is when nonbank businesses offer financial products and services, such as bank accounts, wallets, payments, and lending. Examples of this may include a big box retailer offering on-the-spot finance for large purchases, a pet supplies retailer offering a range of payment options, or a practice management software company taking payments in-platform and monetising transactions.

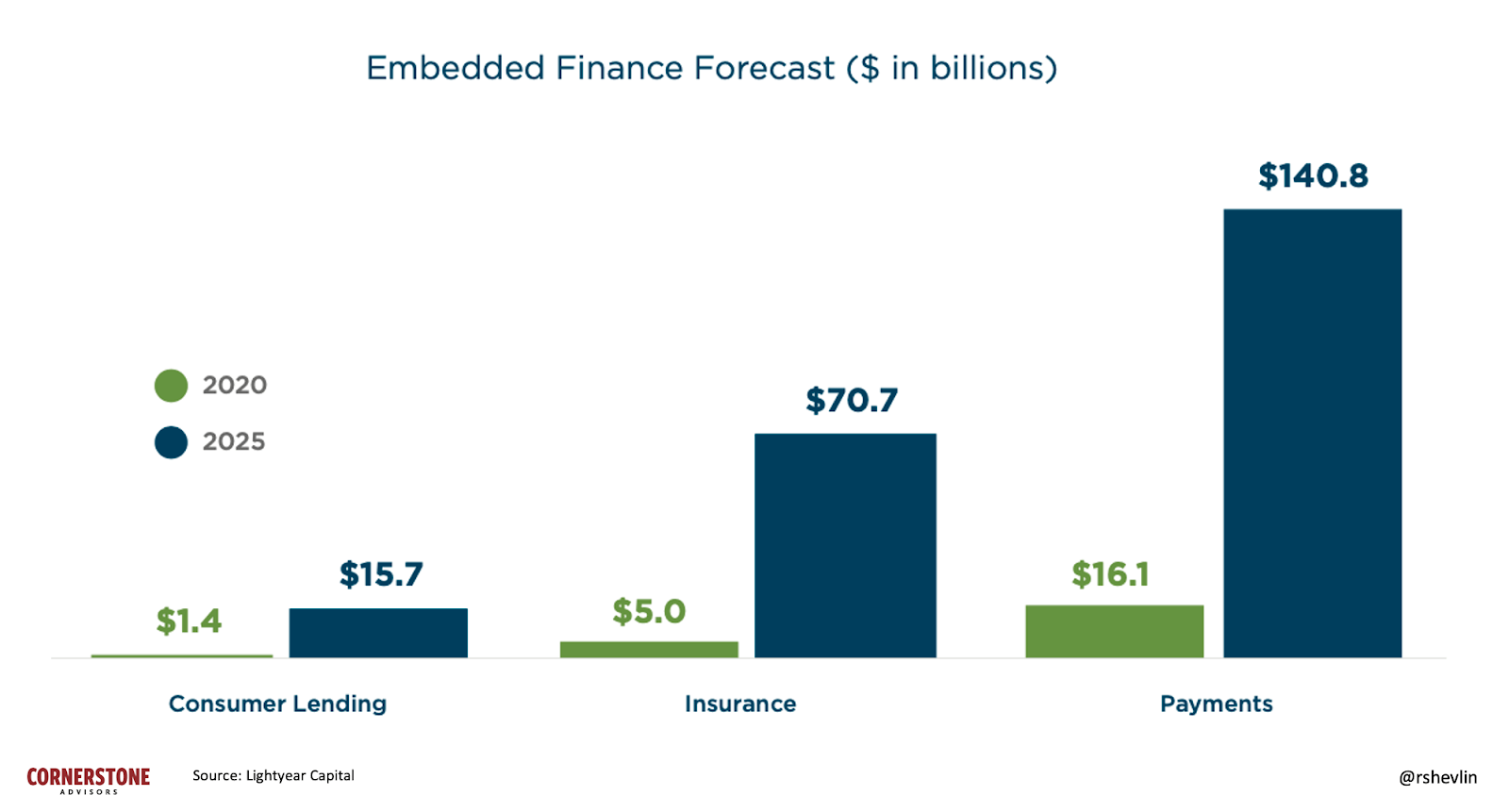

Embedded payments, or Payments-as-a-Service (PaaS) are a key component of embedded finance, and forms the largest part of this rapidly growing industry. In fact, according to Lightyear Capital, payments will account for 60% of the growth of Embedded Finance by 2025.

The reason for the rapid growth of embedded payments can be attributed to the changes in consumer demands, evolving compliance laws, and the wide variety and evolution of viable options for integrating payments into a software platform.

There are three options for integrating payments into a SaaS or software company:

- Legacy integration: Provides some revenue potential with minimal control and customisation.

- Full Payment Facilitator (PayFac): Highest revenue potential with the highest costs, compliance requirements and risk.

- PayFac as a service: Partnering with a provider to grow a new revenue stream while the risk and compliance are largely managed by the provider.

The avenue that a software company chooses for embedded finance will depend on its unique objectives. Whichever option is chosen, there must be a balance between revenue earning potential, managing compliance risk, and a positive customer experience.

Australia’s embedded finance market

According to Research and Markets’ Global Embedded Finance Markets and Investment Opportunities Report 2022, the global embedded finance industry is expected to be valued at USD $777 million by 2029. Representing a compound annual growth rate (CAGR) of 23.9 percent from 2022 to 2029, demand for integrated payments will continue growing in the years ahead.

Unlike more established markets such as the USA, where early innovators such as Uber demonstrated the power of a seamless customer experience, leading to the “Uberization” of many industries, the fastest growth in global embedded payments in the coming years will be in the Asia Pacific (APAC) region.

The fastest growth in global embedded payments in the coming years will be in the Asia Pacific (APAC) region.

From 2022 to 2029, the CAGR for embedded payments in Australia is expected to be 29.4 per cent — 5.5 per cent higher than the global average. Further, from 2017 to 2021, Australia saw a 200 per cent increase in embedded payments. This growth has been driven by changes in purchasing behaviour brought on by the global pandemic, the rise of tech startups and innovation in the APAC region, and changing compliance laws making it easier for financial institutions and fintech companies to innovate.

These changing regulations, demand for cashless payments throughout COVID-19 and record levels of corporate investment in Australian fintech companies shows Australia’s fintech market is reaching new levels of maturity and heading for another significant stage of progression and growth, especially in payments.

What makes Australia’s embedded payments market different?

Outside of regulation inhibiting the development of integrated payments in Australia, other factors make Australia’s embedded payments market different.

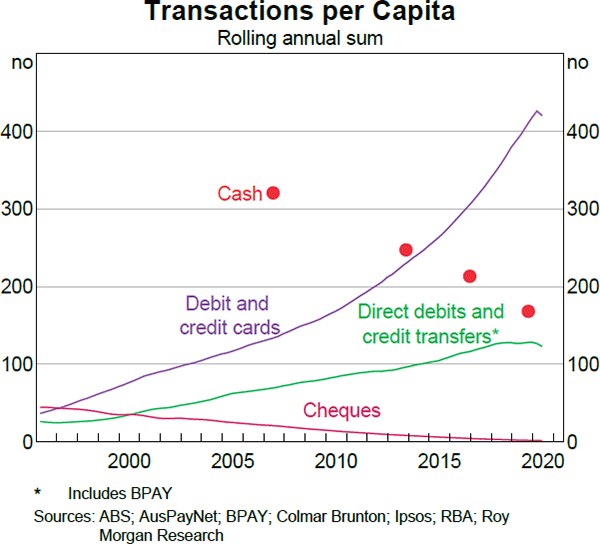

First, cash payments were more common in Australia compared to other western developed economies. This was the case until around 2012 when the use of cash started to decline as card payments grew. In 2012, cash made up 45 per cent of payments in Australia, declining to 20 per cent by 2018.

Source: Reserve Bank of Australia

As the use of cash has fallen, debit and credit cards have become the most common payment methods, equating to over 400 transactions per capita each year. Payment methods such as BPAY, direct debit and credit transfers are less popular than credit and debit card payments, making up around 125 transactions per capita each year.

Similarly, the development of the New Payments Platform (NPP), which launched in February 2018, provided the infrastructure for people to make real-time electronic funds transfers and arguably drove an increase in appetite amongst Australian people and businesses for fast, seamless payments.

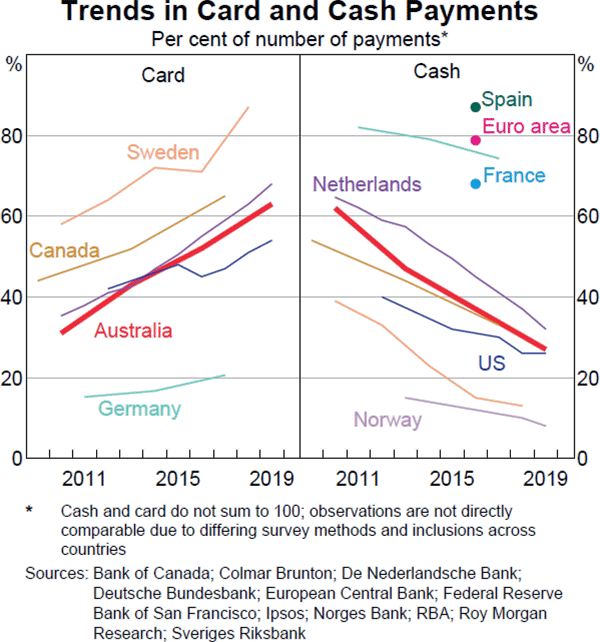

Source: Reserve Bank of Australia

The growth of electronic payments in Australia, along with important changes to our local compliance regulations, has driven a wave of new fintech innovations, some of which are helping companies in industries outside financial services become fintech innovators too.

For these companies, embedded payments present an opportunity to monetise a task that already happens in the business every day — payment processing. In Australia, software as a service (SaaS) and vertically-integrated software platforms, in particular, have a unique opportunity to create a new revenue stream with payments while improving the customer experience.

…vertically-integrated software platforms, in particular, have a unique opportunity to create a new revenue stream with payments…

How does embedded finance impact vertical software platforms?

Vertically-integrated software platforms need strong customer retention to survive and grow. Embedded finance provides an opportunity for software platforms to establish new revenue streams while delivering a seamless customer experience. Further, with ownership of facilitating payments, new types of customer data can be analysed to drive business improvements and growth. Under a traditional payments model, a software company would have access to payment data, but it was limited.

Software platforms stand to benefit from growing customer demand for a seamless, all-in-one experience. According to Bain & Company, embedded finance in software platforms delivers a superior value proposition due to three factors:

- A better customer experience: With integrated payments, the owners and leaders in a software company can use and offer embedded payments while benefiting from streamlined onboarding, integrated dashboards and analytics, and one less provider to manage.

- Savings: Software providers can cross-subsidise their offers in cases where it stacks up. For example, a software company may subsidise discounts on their subscription fees (or remove the fees altogether) due to its payment revenue growth.

- Risk management: Embedding payments provides additional data to assess risk. This allows for easier identification of customers who pose a credit risk or the ability to provide solutions to customers that may not have adequate access to goods and services in the traditional bank-driven value chain.

By introducing embedded payments, a software company can not only generate revenue from payments, but the user experience is enhanced too. This establishes a new value chain where the software platform takes a powerful position, offering customers more value and functionality than traditional payment processors can deliver. The new value chain applies to all kinds of software providers, from gym management software to property management software.

What do software providers need to succeed in Australia’s embedded payment market?

SaaS and software companies are acutely aware of the challenges involved in building technology, so the potential to improve business operations and grow revenue without development costs is a significant opportunity. For example, taking payments in-platform in a SaaS company can increase revenue by 2-5x through a single payments API that offers a range of customisation options.

In a competitive market like the software industry, embedded payments should be an addition to a stable core offering. The point at which a SaaS company is ready to introduce and offer integrated payments will differ between businesses and industries. When it’s time for a software company to monetise its payments, getting hands-on support from a payments provider is critical. Not only does hands-on support make for a seamless transition, but the path to growing through embedded payments is made clear and achievable.

Further, with many businesses using payment tools integrated with their accounting software, such as Xero, software companies must choose embedded payments providers that make integrations seamless. On top of processing payments, these integrations should improve data flows across the business, deliver efficiencies, and provide reporting that will drive stronger commercial decision-making. As SaaS platforms know, it’s no longer enough for a technology provider to deliver operational functionality. Its products should have features that drive strategic and commercial improvements too.

How can vertical software companies maximise the integrated payments opportunity?

Vertical software companies have a significant opportunity to scale through integrated payments. Whether a software provider chooses a front-end-only model, a hybrid model, or becomes a full PayFac, payments can deliver a new revenue stream that grows with the business. Importantly, integrated payments can deliver revenue growth opportunities for B2C and B2B platforms, and the keys to success are largely the same.

In the APAC region, companies value one-stop-shop options, so payments provide an opportunity to simplify payment flows. Simplified flows could mean the ability for customers to choose from a range of payment options and process payments in one menu. Similarly, embedded payments easily integrate the latest security and risk features into the business. These features, such as 3D Secure 2.0, provide extra security and fraud prevention without sacrificing a seamless user experience.

For software platforms to realise the benefits of embedded payments, they should focus on engaging providers that can manage the build and integration process and reduce the compliance burden of processing payments.

Similarly, integrated payments providers should be able to work with SaaS companies as partners in ensuring the user experience is seamless. On top of a seamless payment experience, software companies should ensure their chosen embedded payments solution provides access to key insights and data that can be used to drive stronger commercial decision-making for the company and its customers.

What is the future of integrated payments?

Embedded payments are a new way for software providers to grow revenue while optimising the customer experience. As Australia’s integrated payments market matures, the next stage of progress will likely see more companies taking on the appearance of being PayFacs, rather than using “out of the box” solutions that don’t offer the desired customisation and control that software companies need.

While becoming a PayFac isn’t suitable for every business, those with the scale to manage the risk, compliance and operational requirements to make it run smoothly can take full advantage of the embedded payments revolution.

For those who want to look and feel like a PayFac, without taking on the complexity and risk, payments-as-a-service partnerships will become paramount. Beyond payments, future in-platform fintech developments are likely to involve the ability for companies to offer lending and financing products, such as invoice factoring or banking features.

Embedded payments can provide software platforms with a competitive edge

The strategic, commercial and operational benefits realised through integrated payments present a significant opportunity for Australian software platforms (specifically vertical software providers) to stand out in a competitive market where customer retention and user experience are critical.

By bringing payments in-platform, SaaS and software platforms take a more prominent role in the value chain by expanding their functionality. Not only does this deliver strategic, financial and operational improvements to software platforms, but it also delivers these benefits to customers.

For those platforms with scale and a proven core product, embedded payments fill the demand for a seamless customer experience and revenue growth potential without a costly build.

Embedded payments can make any software platform a powerful fintech player in Australia’s growing ecosystem. Those companies that take payments in-platform now will have an edge that will compound into the ability to offer other financial products and services in the future.

Embedded payments can make any software platform a powerful fintech player in Australia’s growing ecosystem.